Savings account interest rates are still holding up

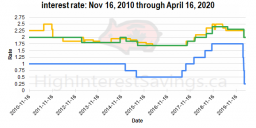

After decreasing the key interest rate by 1.00% in the first 2 weeks of March, the Bank of Canada lowered it one more time by 0.50% to rest at 0.25%, where it has stayed through the April 15 scheduled rate announcement. Although we have seen related decreases to high interest savings account rates across our comparison chart, financial institutions have not yet passed on the full rate decrease via the savings accounts, at least not yet. See this graph tracking the key interest rate against 2 of the more consistent financial institutions for savers over the past 9.5 years (Hubert Financial and Achieva Financial), and how the gap has widened:

Last month, we were musing that we would be lucky to make it out of March with a 2.00% savings account, but 15 of 17 financial institutions on our chart currently have regular savings account interest rates of at least 2.00%. LBC Digital leads the pack at 2.25%, while Motive Financial has the highest TFSA rate at 2.20%. Peoples Trust has even increased its regular savings account and TFSA interest rates from 1.80% to 2.00%, reversing an equivalent decrease from March 6.

Some GIC rates actually increased, if only temporarily

Although GIC rates have generally dropped, several financial institutions increased their rates last month.

Tangerine Bank provided some shocking GIC rate increases by as much as 1.70%, with their 5-year GIC peaking at 3.20%, only to drop back to the middle of the pack a week later.

Oaken Financial had increased most of its GIC rates for about 1 month before decreasing them a bit, settling for what are currently the highest rates on our GIC comparison chart, with a 1-year GIC at 2.50% and 2- through 5-year GICs all at 2.65%. Remember that you can see a financial institution’s GIC rate history by clicking on the links in the “Updated” column on our chart. [Oaken Financial announced GIC rate decreases, effective 5 days after this article was published.]

If you’re looking at the short term, there are at least 2 current 2.45% 90-day GIC offers, from EQ Bank and Oaken Financial. [EQ Bank’s 90-day GIC rate dropped to 2.15% one day after this article was published.]

BC-only credit union Vancity has a promo for a 1-year 3.00% GIC. [Vancity ended this promo one day after this article was published.]

New deposit promos

If you have a Tangerine Bank account, check the online interface to see whether you have the latest 2.80% new deposit promo, which started April 3. They are offering the same 2.80% savings account interest rate for the first 5 months to new clients.

DUCA Credit Union (Ontario only) has a promo offer of 2.50% on new deposits to an Earn More Savings Account between April 2, 2020 and March 31, 2021. They also have a 1-year 2.75% GIC available until June 30, 2020 for customers who currently have funds in an Earn More WINTER Promo Savings Account.

As always, we have a dedicated page to track all known promotions.