Log In

Log In Register

Register Home

Home

Topic RSS

Topic RSS

Facebook

Facebook Twitter

Twitter Email this

Email this5:30 am

October 21, 2013

Offline

Offline

Bill said

I think we can agree that Oaken rates are competitive, they are consistently near the top when all institutions are considered, but they are usually not the highest.

Well, sort of. It depends on how you define '"competitive". Since we're here to find the best rates, in my books "competitive" means the top 2 or 3 in rates for the greatest number of rates. And therefore Oaken doesn't qualify at the moment. They did last year.

Other people are entitled to have their own criteria.

5:37 am

October 21, 2013

Offline

Top It Up said

Perhaps you can provide the link that shows "and it takes them months to pay you". No need for another windy answer, just the direct CDIC link showing the anticipated insurance payout period will suffice.

And perhaps I can't, or, more to the point, don't want to be bothered doing work for you. Why would I?

My comments in #23, in response to #21, are all I am going to say on this question. For those whose concern is genuine, I can only say the proof will be in the pudding. Let's hope we don't have to go there.

5:53 am

December 17, 2016

Offline

Loonie said

And perhaps I can't, or, more to the point, don't want to be bothered doing work for you. Why would I?

Then you should be real careful doling out "spit ball advice" ... particularly if it is no more than another round of FUD, on your part.

As they say "pictures, or it didn't happen."

6:17 am

October 21, 2013

Offline

Top It Up said

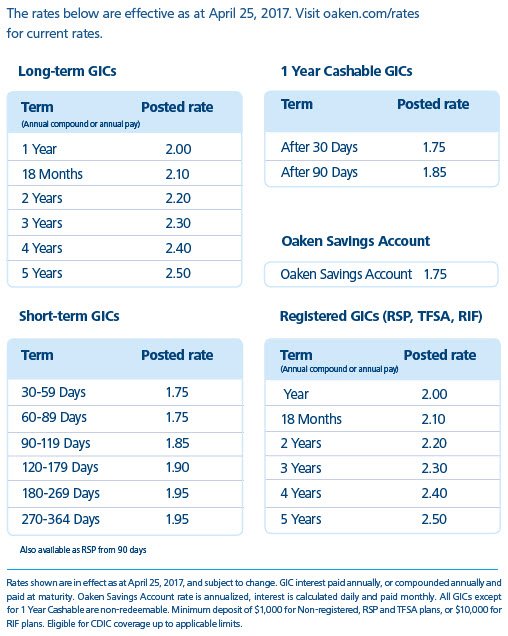

You seem to be a little out-of-touch with both rates and termsFrom Hubert

ONLY the 1-year is not locked and "you’ll [only] earn an average rate of 2.05% for the year (with compounded interest)" IF NOT redeemed

"Any lasting happiness term deposits you purchase after January 15, 2016 are not eligible for early redemption."

"Any TFSA term deposits you purchase after January 15, 2016 are not eligible for early redemption."

"Any RRSP or RRIF term deposits you purchase after January 15, 2016 are not eligible for early redemption."

EDIT: Hubert dropped their 1-year rate this morning.

Yes, they dropped their rate within hours after my post. That hardly makes me "out of touch".

You are only showing selected portions of what they are saying, which, not surprisingly, gives an inaccurate impression.

Anyone who wants to find the full statement can read it here:

https://www.happysavings.ca/products/terms/high-interest-terms/

The changes cited from January 2016 have nothing to do with the one-year term deposits, as is clearly stated.

Don't assume the redemption policy on the one-year term has changed since my inquiry a few years ago unless Hubert tells you that directly.

6:28 am

December 17, 2016

Offline

It would be helpful if you actually read the link you posted.

You were wrong on the Hubert rates long before I edited my post indicating a drop in rates.

8:28 am

October 27, 2013

Offline

Brimleychen said

I think your guy read too much fake news from shorters. Home Trust has been much solid.Please go to TSX or home trust web site to read the official financial informatio. Here is the latest Info:

http://www.homecapital.com/Sup.....Master.pdf

The tier 1 capital ratio is 16.54%, much better than all 5 big banks, because of low leverage. It has abou 1.56 billion in cash holding as of Dec 31, 2016.

Although there is some allegation about discosure of shareholder information in 2015, the business is very profitable. They are still making $4 per share a year, and share price pushed down nakedly shorters. A lof shorters are hiring reporters / news agency to trash Home Trust.

.

Good post re: financials. Keeps things in perspective.

8:36 pm

October 21, 2013

Offline

Top It Up said

It would be helpful if you actually read the link you posted.You were wrong on the Hubert rates long before I edited my post indicating a drop in rates.

I doubt that you find anything that I read to be helpful as you reject out of hand most of what I say about what I have read, including emails from Hubert.

My post about Hubert's rates, #14, was made the evening of April 20.

Hubert changed their rates April 21 as both their email and web update indicate. https://www.happysavings.ca/rates/

You made a post early on April 21, which you subsequently updated to reflect the change in rate.

I think we were all surprised to see the rate drop on the 21st. In any case, it remains better than Oaken's. This was the point, not splitting hairs about dates and times.

2:14 pm

April 24, 2017

Offline

Effective April 25, 2017, our interest rates will be increasing. View our rates here! Desperate much? 4 days after a previous increase?!?

2:23 pm

April 24, 2017

Offline

Norman1 said

AltaRed said

Indeed, I knew better (that deposits are liabilities).

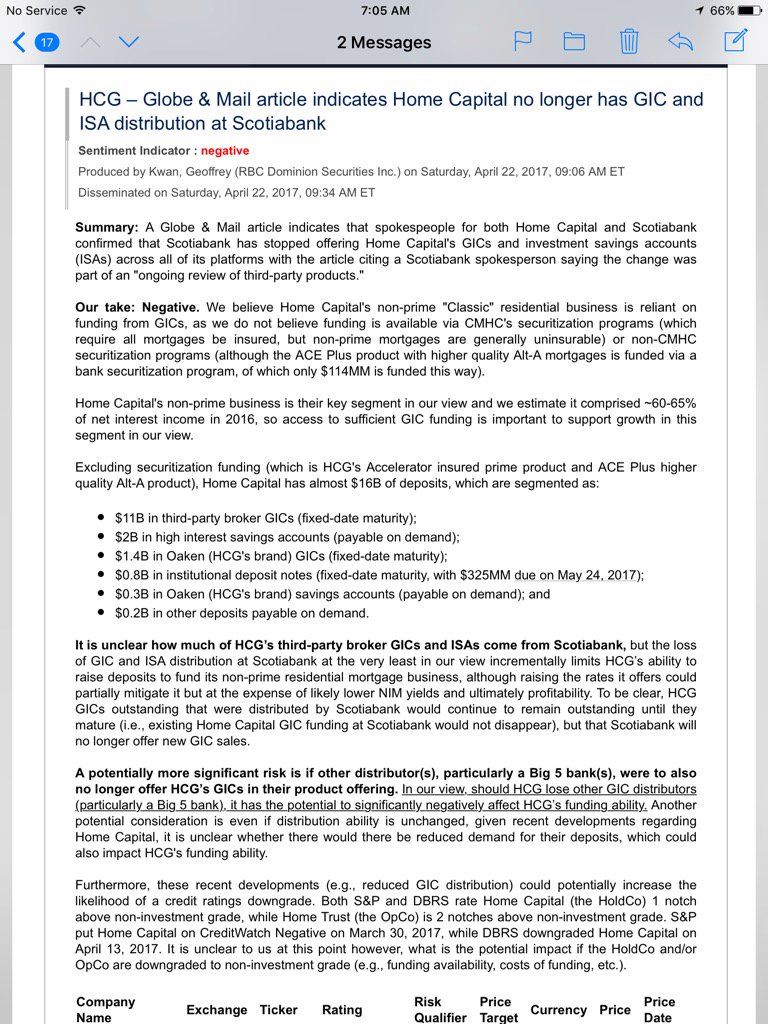

Twitterland is abuzz today with an RBC Research report (noted on StockChase someone says) that says HCG has a need for $325 million (of something) over the next month. Scotiabank (meaning their brokerages like Scotia iTrade) have announced they no longer sell Home Trust GICs (I have confirmed that latter point). …

Any details on what Home Capital Group will need the $325 million for?

Is $325 million what the OSC is asking for as the fine?

Do you see $325,000,000 in institutional deposit notes with fixed date maturity due on May 24, 2017. Where is HCG going to find 325 million in a month? ITS OVER!

2:32 pm

April 24, 2017

Offline

Saver-Mom said

RBC research? Royal Bank? Is that not a competitor of HCG? Is it not in the interest of the competition to cast aspersions on HCG? Should we not question the validity of that source?

Mom, try to understand that HCG will be crashed and soon you will witness a run on the bank.

2:36 pm

December 17, 2016

Offline

Dr_Hubert said

Mom, try to understand that HCG will be crashed and soon you will witness a run on the bank.

ONCE AGAIN for clarity, before anyone starts running to their balconies and wondering if 15 stories is high enough ... that's neither here nor there to depositors within the CDIC limits.

BUT it was nice of the newly-minted forum member, Dr_Hubert, to stop by and share his take on the latest patter concerning HCG.

3:04 pm

December 12, 2015

Offline

Dr Hubert, are you a Hubert employee?

They are naming a new CFO. Also, The Bank of Nova Scotia has advised Home Capital it will resume sales of Home Trust deposit products today, subject to a $100,000 per-client cap.

3:52 pm

April 6, 2013

Offline

Dr_Hubert said

Do you see $325,000,000 in institutional deposit notes with fixed date maturity due on May 24, 2017. Where is HCG going to find 325 million in a month? ITS OVER!

Thanks for solving the mystery about what the $325 million is for.

That means Home Capital needs to have $325 million on May 24 to pay the maturing deposit notes. It doesn't mean they need $325 million by then.

There is a subtle but important difference between "needing to have" and "needing".

Brimleychen found earlier that Home Capital has about $1.56 billion in cash. The $325 million could easily come out of that.

Maybe they can offer the holders of those deposit notes an extra 0.10% too. The noteholders may renew them for another term!

3:57 pm

April 6, 2013

Offline

Dr_Hubert said

Mom, try to understand that HCG will be crashed and soon you will witness a run on the bank.

…

That's just false: Lending for five years using money from one or two year deposits.

Even if Home Capital didn't know better, both CDIC and OSFI do understand what can happen when a lender mismatches the duration of the funding and the loans like that.

3:59 pm

December 12, 2015

Offline

On Friday, a day after they dropped by 20%, shares in the company jumped more than 15 per cent before closing up 8.7 per cent at $19.25.

According to Motley fool today: "So why is Home Capital Group Inc the stock of the year?

For new buyers looking for the ultimate dividend machine with the potential for capital appreciation, Home Capital Group Inc is it. At close to $20 per share, investors will receive a yield of 5.2% while the company pays out approximately 30% of earnings in the form of dividends. The remaining 70% can either be reinvested into the business or the company’s share buyback can continue.

Perhaps some fear-mongering is propagated by those who hope to affect stock prices negatively in order to create for themselves a juicy buying opportunity.

4:35 pm

April 24, 2017

Offline

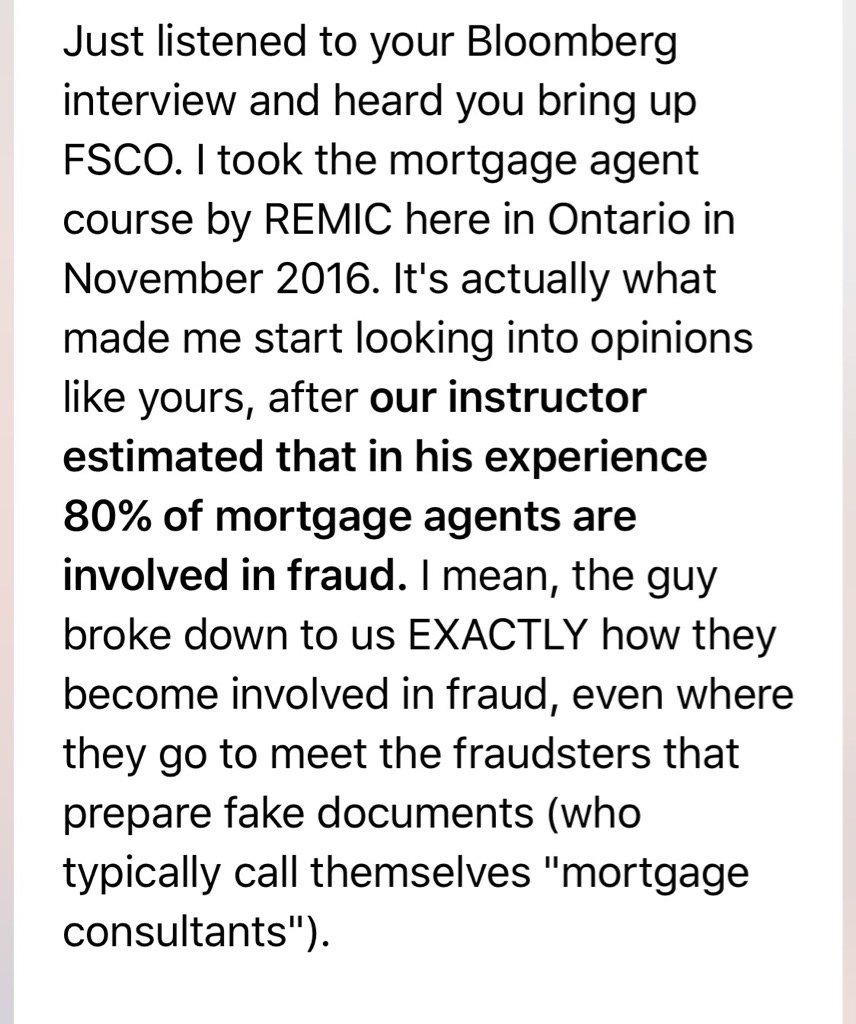

Home Capital Needs to 'Clean House' video on Bloomberg TV:

https://www.bloomberg.com/news/videos/2017-04-24/cohodes-says-home-capital-needs-to-clean-house-video

4:52 pm

April 24, 2017

Offline

HCG business is structurally flawed and people start seeing where the end will be.

4:54 pm

December 12, 2015

Offline

Thank you for confirming that you are influenced by short sellers whose motivation is to see the stock decline.

"Legendary short seller Marc Cohodes has long been Home Capital's most vocal critic." (From the article you quoted in post 56)

5:10 pm

April 24, 2017

Offline

This should get people very very concerned about HCG equity. Where is the bid in this Instrument? Had the same conversation with another investor this morning. Credit blowing out is usually a tell tale sign ...

5:18 pm

April 24, 2017

Offline

On the top of it, Gerry seems like the kind of fella that might pledge his stock as loan collateral too.

Dr_Hubert said

This should get people very very concerned about HCG equity. Where is the bid in this Instrument? Had the same conversation with another investor this morning. Credit blowing out is usually a tell tale sign ...

Please write your comments in the forum.