Log In

Log In Register

Register Home

Home

Topic RSS

Topic RSS

Facebook

Facebook Twitter

Twitter Email this

Email this8:09 am

January 3, 2013

Offline

Offline

Hello, I have never paid to get my score but thanks for those who pointed out the free score report by RBC / CIBC. I used them and found out my credit score is 773.

Is this considered a good score when coming to getting a mortgage? I don't and never had any balance on my credit cards (Always paid fully) and never actually had to use a credit line or loan (I bought all my cars cash - of course not new cars).

I assume this score is because of me opening / closing credit cards once every couple years.

Thanks

8:59 am

October 21, 2016

Offline

Yes, 773 is a good score. and scores in the 700's are very common.

Last year when I opened an account at Comtech Fire Credit Union I was told my score was 840 and that those above 800 were a minority. I had never before asked about my score. Never cared about it.

9:25 am

December 4, 2016

Offline

Credit Score is just a very quick summary of a credit report. For credit cards, it is used heavily. For loan, lines of credit, mortgages they look more at the actual credit report way more than the score (or they should).

Also, Credit Scores are calculated differently by different reporting agencies. Individual creditors might have their own system of calculating Credit Scores.

A Credit Score gives a general idea of what a creditor might be looking at. It might also be off by a wide margin. Basically, I'm saying Credit Scores aren't worth much. Get your Credit Report instead.

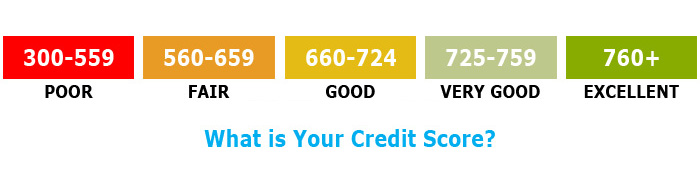

If you know that the creditor is using the same system as the one where you got the Credit Score from, then 773 is Excellent.

http://accessible-mortgages.co.....-chart.jpg

A credit report is still a much better way of seeing if a creditor will extend you credit. For example, you might have a high score and still get rejected credit, if your report contains something they don't approve of.

11:00 am

April 6, 2013

Offline

It depends on whether or not the lender uses the same scoring model.

The free credit score report from RBC has the TransUnion CreditVision Risk Score. That score will not mean much if the lender uses the Equifax Risk Score, the FICO Risk Score, or their own proprietary score calculated from the credit history.

11:21 am

April 6, 2013

Offline

In CIBC Free Credit Score Service FAQs, CIBC provides more information about the free score provided:

What is a credit score? What is a credit report?

…The Equifax credit score* you receive through CIBC’s Free Credit Score Service is a 3-digit number, between 300 and 900, calculated by Equifax and based on information in your Equifax credit report. This credit score is offered for educational purposes, but may also be used by CIBC, together with other information, to offer you credit products and services. It won’t be used by CIBC to evaluate an application for credit.

…

*The Equifax credit score is based on a proprietary model owned by Equifax and may not be the same score used by third parties or CIBC in certain instances to assess your credit worthiness.

9:10 pm

January 3, 2013

Offline

Thank you everyone. Even though, I don't really care about it at the moment, I'd like to see it above 800 (Just for fun!). Let's see if I can make that happen!

3:24 pm

May 28, 2013

Offline

I herar that one way to increase your credit score is to take out a loan, and then immediately pay it all back. Do this a few times and you look like a great credit risk.

Of course, also pay off your credit cards and any bills before they are overdue.

That said, credit scores for people who do not have any debt (such as loans or mortgages) often look relatively low (in the 700s). I have not had debt for years, pay all bills on time, yet my score is below 750.

4:56 pm

September 11, 2013

Offline

I suppose having a pattern of regularly taking on debt and subsequently meeting all obligations might be considered a safer bet than someone who doesn't have much of a history with debt.

5:00 pm

October 21, 2013

Offline

I think it's all a bit of a racket, really. You have to take on loans, whether you need them or not, and pay unnecessary interest, when you may have gobs of money of your own, just to satisfy these people that you're a good risk for a credit card?

9:26 am

September 11, 2013

Offline

I think most of us on here would be pretty careful before we loaned our money to a stranger. And I'm sure we'd also expect an fi where we keep our deposits to do their due diligence before they loan it out.

12:43 pm

October 21, 2016

Offline

FWIW, I never had a mortgage in my life. Never paid a cent of interest on CC, we own our house and it might be worth more than you think. I have zero debt, never had any debt in my whole life. My spouse is in similar situation. Our scores are 840 and 810.

P.S. We didn't ask Comtech to tell us our score, he provided the info without us asking. He was a real gentleman and very pleasant to deal with.

2:45 pm

February 24, 2015

Offline

Loonie said

I think it's all a bit of a racket, really. You have to take on loans, whether you need them or not, and pay unnecessary interest, when you may have gobs of money of your own, just to satisfy these people that you're a good risk for a credit card?

I'm with you. For over 40 years, I have had credit cards, mortgages, line of credits, investment loans, etc. It is only in the last couple of years that I heard the term 'credit score'. It is not like there is one universal score, right?

8:49 am

October 21, 2016

Offline

A small correction to my previous post; after university I had about $30K in student loans that were paid back within 2 years. And the same for my spouse. I had forgotten about it as it was a long time ago.

6:25 pm

November 21, 2015

Offline

Transunion credit bureau routes calls to India. Only for your information, so you don’t freak out as I did. It is legit, not a “stolen phone number”. The reps (two) were reading of a scrip, that did not correlate to my question, which prompted me to ask about their location. India. Did not feel comfortable going through the identification process. Could you spell “Toronto”? With one of the reps I was not able to communicate due to language barrier on her side.

5:38 pm

February 18, 2016

Offline

Never had any debt; pay CC on time in full; mortgage paid in less than 5 year about 20 years ago.

Current credit score: 845; in June 2017 was 829. Did I do anything (loan, late payments, new CC, etc.) between 2017 and today? No.

So credit score is the same as Tangerine's 'offers'. Random number or as I like to say plain BS.

6:53 pm

April 6, 2013

Offline

SavingIsGood said

…Current credit score: 845; in June 2017 was 829. Did I do anything (loan, late payments, new CC, etc.) between 2017 and today? No.

So credit score is the same as Tangerine's 'offers'. Random number or as I like to say plain BS.

There was a change. Probably a change in loan or credit card balances that changes the percent utilization of total available credit. However, such small changes or differences in credit score are not meaningful.

In a previous post, I mentioned Globe & Mail article What qualifies as a good credit score? A woman was surprised to find her boyfriend had a higher credit score of 846 than her score of 783. She wondered what she did wrong.

An Equifax Canada vice-president explained that the difference in scores is not meaningful to lenders and that lenders consider any score above 700 to be excellent.

6:57 am

October 21, 2013

Offline

It seems to me that in the arcane world of credit scores, even doing nothing counts as activity.

If you had been spending X on credit cards or taking out Y in loans, and then you stopped, that would change your score, from what I can figure out.

8:48 am

April 6, 2013

Offline

Definitely possible.

Paying off the credit cards and loans would cause utilization to fall to 0%. That would increase score. Also, as months pass, the length of one's credit history increases. Longer positive credit history also increases score.

But, such credit score changes are not necessarily meaningful. As in the Globe & Mail article I mentioned, dropping from 846 to 783 would not be meaningful as far as lenders are concerned. There is no statistically-significant change in the default rate between people in that range.

Sort of like no meaningful change in frostbite risk when the temperature drops from 30°C down to 9°C.

3:14 pm

January 3, 2013

Offline

Thanks everyone. I asked this question long time ago. Haven't yet applied for a mortgage (Hate the idea of being trapped in a house I own, I know I know) but between applying for couple credit cards my score has been hovering between 760 and 820. For now, it shows 798 and I applied for Canadian Tire Elite MC. It is pending for now.

4:47 pm

October 21, 2013

Offline

I was told recently by a 35-yr veteran of the banking industry that the highest she'd ever seen was 890. Have to wonder what happened to the other 110.

I'm sure we'll all be comforted to know, when suffering from 30 degree frostbite, that 9 degrees wouldn't be any worse.

{kind=link}

Please write your comments in the forum.