Log In

Log In Register

Register Home

Home

Topic RSS

Topic RSS

Facebook

Facebook Twitter

Twitter Email this

Email this2:35 pm

December 12, 2008

Offline

Offline

Yes, please feel free to list the financial institutions and the type of accounts you have in each.

Would like to know how many accounts the average person has and if you can tell me why you choose to open that account.

djino

12:28 pm

March 25, 2009

Offline

HSBC Direct Savings - Opened due to HSBC offering a +1% promo rate. Will look at closing account in future due to high bank fees. (like depositing US checks = $2.50 s/c each). 0.8% interest rate, etc.

PC Financial Savings & Checking - Opened due to PCF offering no fees and good interest rates. Lots of good freebees like PC Points, free checks, etc.

Mike

Have a great day

3:01 pm

djino said:

Yes, please feel free to list the financial institutions and the type of accounts you have in each.

Would like to know how many accounts the average person has and if you can tell me why you choose to open that account.

HSBC Direct Account -- my primary account since the only thing I can't do with it is write cheques. I opened it because it has no monthly fee, pays interest (though not as much as I'd like these days), has unlimited electronic fund transfers/bill payments and ATM access, and Citizens Bank shut down so I needed to change my primary bank account as a result. Since I rarely use cheques it's perfect for me, and when I do need cheques I use a Mastercard Cheque after pre-paying the amount on the Mastercard to avoid interest fees.

HSBC Direct TFSA - which is now-nearly-empty as their interest rate is too low and therefore not competitive any more.

I have an HSBC Business Direct account to keep my small business cash separate from my personal cash.

I think I'll eventually open an HSBC Performance Chequing account (it would NOT be my primary account as it pays no interest) because I write more cheques than I realized, but haven't decided for sure yet as their $4,000 minimum balance to waive fees is too high in my opinion, not to mention zero interest. I'll probably wait as long as possible until I need a bank draft or some in-branch service before opening one.

Ally High Interest Tax Free Savings Account -- This is where I put most of my yearly savings outside of my pension plan/RRSP since I like the high interest rate (more than double what HSBC Direct offers), ease of use of the online system, and have linked it to my other accounts.

Ally High Interest Savings Account -- Have one of those too in case I go over the TFSA yearly limit.

ING DIRECT -- I have their High Interest Savings Account and TFSA but currently just keep a few dollars in them. I opened these accounts years ago. The only reason I don't close the accounts is I want to see if their interest rates increase over Ally's in the future, but so far I favour Ally as they don't seem to do the bait and switch that ING DIRECT does with teaser interest rates that later go down too low. I like ING, but their rates are not high enough.

Credential Direct Online Brokerage Cash Account - for my self directed RRSP (mutual funds and stocks). I originally used them as they were associated with Citizens Bank and keep getting voted best online brokerage. No complaints.

Citi Petro-Points No Fee Mastercard - my primary personal card so I can build up Petro Points and I redeem the points every December for enough airtime to cover my Petro Canada Mobility cell phone service each year. I love that. It's like I have a free cell.

BMO 1% Cash Back Fee Mastercard - I use this for my business purchases to keep it separate from my personal expenditures. I also use this card for the rare personal cheques I have to write as there's no fee for Mastercard cheques and if I prepay there's no interest charge either. I also like the CAA style auto service I have on the card as it's saved me once already from a dead battery.

Citizens Bank Shared Interest No Fee VISA - I have this as a relic from when I used to bank with Citizens Bank. I don't really need or want it, however, once in a while a store does not accept Mastercard, so it's there just as backup. I only have automatic monthly charitable donations going on this card, just to keep it active.

I also have an employee stock purchase plan account through my employer where we get 3 stocks for the price of 2.

5:53 pm

December 12, 2008

Offline

Very nice Prag!

I also use HSBC for the same reasons as you wrote, and use MBNA's Platinum Prestige Line (Mastercard/Line of Credit) as a backup for Cheques as they provide it free with no service charges and I'd just need to prepay what I use to avoid interest charges.

Although I also have the Citi Points Points Mastercard, I do not use it at all really since about a year ago MBNA came out with their Smart Cash card which gives 3% Cash back (5% during the 1st 6 months) on Gas/Groceries and 1% on everything else. This gives a better return than the Petro Points Mastercard. I believe Citi-Petro is only better when gas falls below 65 cents/litre as you'd save more than 3% (2cents / litre) at the pump. So I use Smart Cash at Petro Canada along with my regular petro points card instead or until gas falls below that price/litre.

djino

12:46 am

bank #1

scotiabank - the first bank i opened my account. it was a choice between TD Bank vs. Scotiabank then but I choosed scotia because i thought they require less minimum balance. it turned out they require higher. hahaha. that's what you get when you dont do your research seriously. well, scotia is a very nice bank. because very low interest rates and high bank fees. hahaha. actually im just observing this bank. i plan to move all my money away from scotia when i have more money like $5000. ahh dream on. but right now, i'll stick my few hundred dollar savings with them. FOR THE MEAN TIME, of course.

bank #2

coast capital - less bank fees. i kinda like this bank. actually they even have no minimum balance requirements. but lately in the battle of TFSA, coast capital TFSA = 1.00% and scotiabank TFSA = 1.25%. im now confused which to bank my tfsa.

bank #3

-i guess ING? or canadian tire. im not sure. but i might try them soon.

1:59 am

December 12, 2009

Offline

I currently having the following accounts with the following institutions. I am also enclosing whether or not each does a "credit-related" (hard) or "non-credit related" (soft) inquiry on your credit bureau. It seems to me institutions that just offer high-interest, "virtual" savings accounts and TFSAs generally do soft checks while those that offer day-to-day transactional accounts generally do hard checks.

HSBC Performance Unlimited Chequing Account (waived service charges due to staff status) - keep an average balance of about $300.00 in it

HSBC Advance Savings (x3) with average combined balances of around $1500

HSBC High Rate Savings (GBP) (waived service charges due to staff status) - opened a couple years ago when the GBP rate was what I thought was good at 1.85. It's now down to around 1.55. It's only about 1000 GBP but I don't want to sell it because I don't want to take the $300 haircut.

HSBC Advance TFSA with $5000 in it

HSBC Mutual Fund RRSP (current market value as of 23MAR2010 $3700)

HSBC Canadian Stock-Indexed GIC RRSP ($1000)

I also have a Scotiabank Gain Plan savings account with $250.00 in it. Kept it because it was almost my very first account - used to have a Kelowna and District Credit Union (now Interior Savings Credit Union) Fat Cat Savings account when I was a wee child but that account's long since closed.

I also have a Scotiabank No-fee Scene Visa for its fabulous movie ticket and concession rewards with Cineplex. I wish they'd expand it to include Landmark Cinemas so I could utilize the theatre in West Kelowna instead of the one in Kelowna. I've racked up quite a number of points already, through initial sign-up bonus points offers and a very generous 4000 points for pointing out some spelling mistakes Scotia Credit Cards sent out via direct mail and already redeemed 5000 points. I still have almost 15000 points though.

Finally, I have two Ally High Interest Savings where I keep my savings currently held in cash and not in a registered plan or invested in Canadian equities, which I use Scotia Capital's TradeFreedom service for (I own shares in TD, CIBC, Scotiabank, Yellow Pages Income Fund and TransForce) although I may move to HSBC InvestDirect.

Ally uses soft credit checks for account openings whereas Scotiabank and HSBC both use hard credit checks.

I checked with several institutions and ICICI and ING confirmed to me they use soft credit checks. Coast Capital Savings does a hard credit check as does PC Financial. I've not heard back from Canadian Direct Financial. I also have not e-mailed Achieva, MAXA, Outlook, Peoples Trust or Canadian Tire Financial Services. Any experience with them? Hard or soft?

Cheers,

Doug

12:34 am

December 12, 2009

Offline

Update 24MAR2010: I got replies back from Canadian Tire Financial Services and Canadian Direct Financial. Both indicated they do inquiries with consumer reporting agencies but are of the variety that don't impact credit or beacon scores, which I take to mean as "soft" checks. I'm going to clarify that and will update you all further.

I'm going out on a limb to presume VanCity does a "hard" check. Can you confirm this, Peter? As for Peoples Trust, Roc, can you confirm if they do a "hard" or "soft" check? Anyone with information on the Manitoba credit unions with virtual bank operations nationally?

Update 25MAR2010: Both Outlook and Achieva do "hard" checks on your credit file. Don't know about Peoples Trust. I wouldn't open an account with them anyway - they're sketchy, I think, and don't offer online banking. What kind of bank doesn't offer online banking? It's actually less costly to offer online banking than require faxed transfer requests from customers or mailing of paper statements via postal mail. I think Peoples Trust execs have their heads up their butts, if you ask me. 🙂

Cheers,

Doug

7:28 pm

May 15, 2007

Offline

I've asked Vancity about what kind of check they do and will report back when they respond.

Update: official response from Vancity is:

"Please note that the credit score performed by our staff is a hard check (in that it would indeed appear on your beacon)."

10:19 pm

December 12, 2009

Offline

Thanks, Peter. Much appreciated! The only one I'm unsure on is Peoples Trust. Perhaps Roc would be best to ask this one? Roc?

Cheers,

Doug

10:09 pm

banking experience #1; something awkward (this is a true story),

i go to my coast capital bank [no.3 road] basically to deposit my paycheck and encash some money too. this usually happens automatically. and this happens for 3 months without any problem, i got on my bank statement a new balance when i use their ATM machines and got some cash from the teller. anyway, the check i am encashing is from the same bank (coast capital check) only my bank is at no.3 road and my boss' bank branch is on no.2 road (no.3 and no.2 roads are in richmond, bc just in case you're wondering)so that should not really a problem because its from the same bank and thus that 3 or 5 day check clearing period should never exist. anyway on my 4th month, for the first time, i tried to go to my boss' bank branch itself and cash there the check while i get some money. and lo and behold something awkward happened.

so here i go. i told the teller, im going to encash my check and deposit some part of it just like i do all the time. and guess what the teller said?

"there is a hold on this account..." so i can't cash the check but instead she will make a withdrawal slip for me to fill so that i will withdraw cash from my old savings account and for the whole amount of the check will then be deposited in my account and i will get a new balance amount on may 4. that day was apr 28. so i was kinda surprised. so i asked where, well, is this check i am holding an "NSF" check? she said "no. the check is okay." what's the problem i cant cash it then?

"its because there was a hold..."

im not really in the mood to have a discussion with the teller so i just do it and left with the questions in my mind. first of all, the check is being drawn from the same bank and not from two different financial institution, and the irony, FROM the SAME BRANCH the check come from so hahaha so they will know if that check tanked or not right? so what do they mean by there is a hold? that's a payroll check. it's for daily survival and spending.

oh whatever..

is that young lady new at her job, she doesnt know what to do?

do i look like a crook she can't trust my face, she thinks i stole the check?

--then why not call the man who issued the check to me, right?

--i showed her my bank card + icbc ID so she doesn't have to worry.

--did the bank just hold on my deposit so that they can save interest on my account, and just credit the amount after the computation of interests? remember that's apr 28 and it will be credited on may 4(what gives? i am not depositing a check worth thousands or millions of dollars but only a couple of hundred. interest computed is not even more than 10cents)

--i really don't know what the crap happened like that.

--i hope i can get another overtime at work so i have another check so i will

go to that bank and deal with it for the second time around. why can't she cash in a check drawn to the same bank if that check is not NSF? something fishy...

if next time i go there and they give me again this reason, i am not gonna just believe them anymore. i need more explanation.

(maybe "Doug" [whom i believe works in a bank] can explain why did that happen? "Doug" are you there???)

1:17 am

December 12, 2009

Offline

I'm a little confused by the scenerio. Did the CSR at the Coast Capital Savings ("CCS") branch explain the funds in the account on which your employer writes its payroll cheques were held and lacked available funds in which to cash your cheque? If this is the case, that's a perfectly valid scenerio and means the CSR did her due diligence in checking for stop payments and available funds in the CCS account on which the cheque was drawn.

If, on the other hand, the CSR refused to cash your payroll cheque (drawn on a CCS account) because your account had a hold on it, that should have no bearing on the ability to cash the cheque (since the cheque is drawn on a CCS branch in which the CSR can check for stop payments, verify proper signing authorities and available funds). The CSR can only restrict your access to the held funds in your own account (if, for instance, you were trying to withdraw all of the money in your account including funds that were not immediately available to you). If this is the case, I would refer the matter to the branch's Manager Customer Service (or similar title) and, if you still don't see it resolved for future cheque cashing situations, ask for a copy of their customer complaint resolution brochure outlining the next steps available to you.

Hope this helps,

Doug

4:56 pm

thanks for the reply Doug. yes, i did ask the CSR at CSS and she said there is sufficient fund [duh. but why can't i cash then?] in the account only that there is a "hold" i dont know what kind of hold is that because it's sure HOLDing like a real pro. note that the check is ready-to-go meaning its not post dated or anything. it's just that the hold is unknown. anyway, i checked my balance now and yes, it's already updated to the account balance i am expecting.

next paycheck, i will not go to my CSS branch but instead go again there at my boss bank branch and cash my check, see what will happen. im so excited. if this crap happens again, i will make a major rant. hehehe. not really.

ok, change topic:

hey, guys i just had my scotiabank card activated for online banking and wow, after checking the website, what a disappointed. scotiabank's online banking is like, what is this!!! so bad. for scotiabank to be a part of the BIG 5 in canada's banking is a major joke when you check their online banking. where is your R&D scotiabank? the user interface is just soo basic, you can't even have transaction history or summary. it's just that -

your account balance is $xxx.xxx. the end.

in the user interface. i rate their online banking user interface 1 out of 5.

while coast capital will go 4.5 out of 5.

12:15 am

December 12, 2009

Offline

I would agree with you that Scotiabank's Internet Banking is poor when compared to its peers. Having said that, they do allow you to view your cheque images online which HSBC does not currently. There's pros and cons to both. Haven't used other banks so really can't comment.

With regards to your other issue, it sounds like your boss' account may have sufficient funds in the account but they weren't "cleared" funds (meaning ready to use or available) and so that's why she couldn't cash it for you.

How is your credit rating? If it's sufficient, your bankcard may have limits in place such that it allows you to deposit money at an ABM and receive same day credit on all or a portion of it, allowing you immediate access to the funds. That's one avenue. A word of caution, though, if the cheque is returned to your account as "funds uncleared" or "NSF", you are responsible for any overdraft it creates, as per Canadian Payments Association (the cheque clearing system operator) rules.

Cheers,

Doug

5:34 am

my mistake for giving a low review on scotiabanks' online banking. as it turn out, i was just stucked at the "home" tab, and explored there endlessly. where there is really no information you get but your balance. there are generally six tabs, that's

[home][banking][investing][borrowing][insurance][planning]

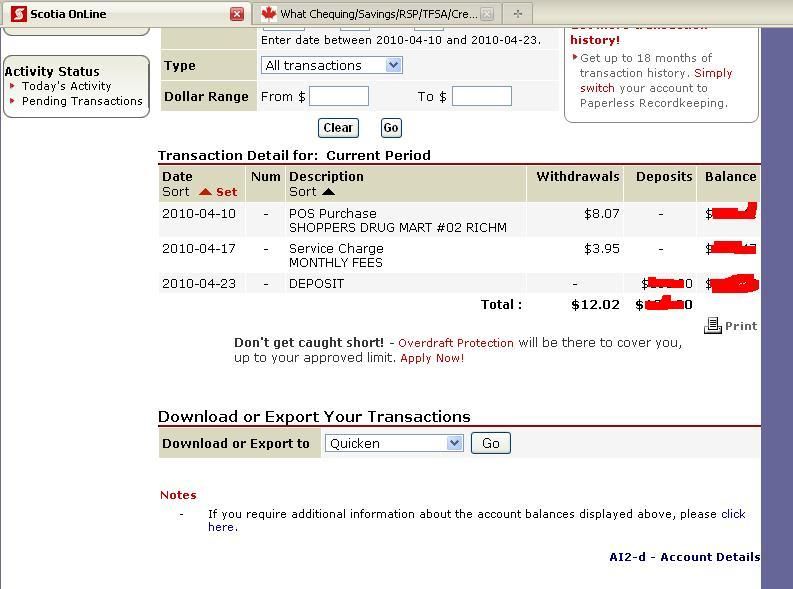

now click on [banking] and there are more options to look forward in your "account information" click "account details" and their goes the information we mostly need to know, the Account Transactions Summary, similar to this, check it out:

http://i1038.photobucket.com/albums/a461/20503618/scotiaonline-1.jpg

so this is good actually. now we can see more details about what we did with our money. this is very important, imagine if your a victim of identity fraud, you can actually see what/where/when did that crook did with your money with transaction detailed like this.

i take back the 1 out 5 rating. that is not right. although the site is not much user friendly, it still does its job. my rating of scotia online should be 4 out 5.

4:53 am

okay dokay, so after receiving my paycheck, i went again

to coast capital no.2 branch... yes, again to that bank and not my branch.

and same strategy, cash out the majority,

deposit the rest. so what happened?

well, just as i signed my check, the guy

said, "because im a new customer... i have some hold..."

ME: "Again... what is this "Hold" bugging my life again...

but he later retracted his statement and said, it should be fine.

so i got what i wanted. im about to fire up and ask him a lot

of questions if why they put some unknown HOLD again.

but since all is good. no need to talk. just say thank you and

leave.

5:37 am

hi doug,

how are you?

this letter is for you. i want to ask some questions basically.

[since you work at a bank...]

story:

I opened a savings account. I made an automatic monthly transfer and

withdrawal for my TaxFreeSavingsAccount and a charitable organization.

Question: What if my savings account ran out of money [which will

happen in the event of loss of job or no money being deposited, right now its

just $40.xx ouch! It needs to be at least $360 every month to be "safe"] and then those automatic withdrawal kicks-in? Will my bank charge a penalty for me? I know, I should ask my bank for this, but let me ask you first, how does your bank handles such situation because it might happen.

And I guess this often happens in lots of banks....

1:03 am

December 12, 2009

Offline

Automatic monthly contributions from your bank account to a charitable contribution are a form of Electronic Funds Transfer (EFT) (essentially, electronic "cheques") and are called pre-authorized payments officially or informally, direct debits. If you don't have sufficient funds in your account the date it withdrawn, the next morning it will show on a bank's exception reports and likely your account manager will call you to come put money in your account by 10 AM that day or the payment will be returned as NSF and an applicable service charge may apply. As well, the payee may charge you a fee on their end as well (charitable organizations generally don't, since it's not an obligation that you owe them money, it's a donation but check with your pre-authorized debit agreement with the payee).

Hope that helps,

Doug

5:17 am

i went to a scotiabank branch and open up a new TFSA account. though most books that i have read about TFSA says its better to just have one (1) TFSA account for easier administration and yes, i already have a TFSA account at coast capital but just trying to see the difference of these two. so what's the story?

oh well, it took about an hour for me to get finished. just for that. actually the lady said i need to set-up an appointment first (and like, this is my day-off hello? the only time i'm gonna be free again is 6 days after today) so i'm about to leave and abandon mission when she asked me if i'm already a scotiabank customer (which i find it redundant because all people who go inside the bank should be a customer per se right?) so she asked my scotiacard and i gave it to her then she went inside in one of those cubicles and after 30 seconds she came back and said, one of their officer is free so he can assist me.

i really dont like handling my debit card to anyone and not seeing what is really happening with it. i know im inside a bank but hey, what if something fishy is really happening while the debit card is out of my sight. its not easy to trust anybody these days. even a bank employee can have a portable credit/debit card skimming machine you know! hehehe!

anyway, back to the story, so the guy told me the basics about TFSA. Of course I pretended to be interested listening but after reading 4 or more books about TFSA, im not really listening anymore. because it's rude for me i think, to say, "i know. i know. i know." so i let him finish his talk.

basically, my address in my scotia account is still at Toronto. And he demanded that i change it to my current address here in Richmond, BC. I just told him, my residence address remains at Toronto then mailing address here at Richmond but he explains if ever there is problem, its better if i change it to Richmond then if I return back to Toronto then I change my address again. So since I can't convince him to stay put with my old address, okay, let's use my current address which is Richmond and so we changed it on the computer. While he is updating my records as I showed him my driver's license for my address, we talked about the World Cup. And I asked what is his team, he said Korea. Wa ha ha. I feel kinda scared now. I hope its South Korea and not North Korea. hahaha! Oh well, he's for south korea. Then I asked him what's the update with the match. and he said, they have a game. And so, while updating my address on his computer, he launches a new web page, to where but where? World Cup website and for me it's like. WTF. By a simple error or webclick, you can get malware, spyware, virus, trojan, syphilis (joke!) with what you're doing man! And you're exposing me too. My record is open just on another tabpage with my birthday, SIN, favorite color, favorite song, etc. Oh come-man, what you're doing is dangerous.

Anyway, after that, [at this time, im not so impressed anymore with this undertaking] so signed the application papers for the TFSA and man, check out the papers. I kinda like the Coast Capital TFSA application. It's more professionally crafted. The Scotiabank paper is so so. Then after giving the money, I asked him, why is there no "successor account holder" or at least a beneficiary designating paper that I have to sign. Come on, if i get hit by a bus and die, at least i want to transfer my estate clear, easy and tax-free. This is no problem with coast capital at it's already part of the application document, but with scotiabank, there is none. You have to explicitly ask for it because its not part of their TFSA application document. And so he kinda scrambled and look for that document, read the guidelines for himself at the screen and printed it. Because I don't know the SIN of my spouse (i have the number at the house) he decided I will then have to come back another day and complete the paper. (To set up a successor hold, you need the name and SIN of your spouse) And then he gave me an investment guideline book made by scotiabank. The end.

TFSA have been around for quite a few years already. 3 years I guess. So I'm a little surprised how come our friend at scotiabank seemed not prepared at all. For sure, he must have prepared hundreds of this similar kind of transaction already. then after reading that investment guideline he gave to me, he missed to print me my Declaration of Trust. hahaha. I checked my coast capital TFSA docs and yes, there is a document of such. Man, our scotiabank guy must be soo hyped about world cup.

So overall my comparison,

TFSA documentation- Coast capital wins. Scotiabank is so so.

TFSA bank employee skills- Coast capital have more people knowledgeable i guess.

TFSA completion time- Coast capital makes it faster to get done.

TFSA Rate- Scotiabank Wins! 1.5 per cent compared to Coast Capital of 1.0%

10:54 pm

just came back from scotiabank [got to leave at work early just to catch this stupid "banking hours"] and set up my "successor account holder." i am not really impressed with this guy who opened my TFSA account. because i have a lot of talk and question with him, he told me, i am the only one he met that actually read the scotiabank investment book/guideline that he gave me. hehehe, what that does mean, he never actually read the book? of all the people, he should be the one who mastered that book. that is part of his job as a, let me read his card, as a "personal banking officer." i asked him about the document, declaration of trust that must be part of my application document package as it is said in the book. then he scrambled on his computer (google's help!) looking for some info about that document. he convinced me that i don't need that document as that document is only needed if my TFSA is bound to mutual funds! my TFSA is only "cash" basis. is that so? but the book never said anything about it. anyway, so i finished signing up my successor account holder and left. then i realized, i missed my copy. he should have given me a copy. or do i need to explicitly ask about it? shouldn't this transaction be automatic? i should have a copy at least to prove in later years that i did set-up an successor account holder. what kind of proof do i have at all without my own copy. but, really, i don't want to spend more time with that bank. it's just not happening the way it should be. im annoyed partly at least. i think i can do a lot better job than this guy. maybe he is just a new employee hence very amateur in his job performance or maybe i expected a lot from him. anyway, my advice if ever you set up a TFSA account in any bank/financial institution, expect the following to be at least accomplished for peace of mind:

a.) TFSA application package

b.) declaration of trust document

c.) successor account holder/beneficiary document setup

if the person who works with you is giving you a hard time doing those basic

things then there is no need to pursue coz they bring you a lot of headache and waste of time.

1:25 am

December 12, 2009

Offline

Without knowing specifics, a few things I have to comment on. First, bank employees do NOT skim your debit card to create duplicates. Remember, they work in a bank. And, in the event someone was a crooked employee, they would not need your debit card to make fraudulent debits from my account - see my point above about them working in a bank. They're bondable employees, with thorough criminal records, credit and background checks done prior to hiring.

Second, the employee probably had his web browser's home page set to the "world cup" webpage likely because he's a fan. If anything, I think that brings him down to earth and makes him approachable.

Third, without knowing the type of TFSA you were wanting to open, because it's registered with the Canada Revenue Agency, the bank is required to ask for your SIN. You can decline it but, as per the Income Tax Act, the CRA can fine you at least $25.00 for failure to provide your SIN to a financial institution on any registered account. It's required for regulatory reporting purposes. You can still decline use of your SIN for marketing and/or credit reporting purposes, however. As far as updating your address goes, if he's based in BC your address shows as Toronto, depending on the type of TFSA you're opening, there are regulations that prevent an investment advisor from selling investment products to clients in another provincial jurisdiction despite them being face-to-face. It's an MFDA (Mutual Fund Dealers Association) prohibited selling practice and doing so can result in disciplinary action which could include suspension or termination of an investment fund sales license.

Hope that helps,

Doug

P.S. If all you're wanting is a TFSA savings account (not mutual funds), you should be able to open one online through ScotiaOnline as an existing customer. Open it up online then return your beneficiary designation to the nearest Scotiabank branch. As well, you can't designate a successor holder if it isn't your spouse. You must use beneficiary.

{kind=link}

Please write your comments in the forum.