Log In

Log In Register

Register Home

Home

Topic RSS

Topic RSS

Facebook

Facebook Twitter

Twitter Email this

Email this9:18 am

February 14, 2023

Offline

Offline

We’re writing to inform you that on February 4, 2025, the following interest rate changes will take effect for EQ Bank accounts:

Please note, only the rates listed above are changing. To view a complete list of rates for all our products, visit our Rates Page.

Why is EQ Bank changing our rates?

The Bank of Canada has continued to lower interest rates as inflation stabilizes. On January 29, 2025, their benchmark interest rate was reduced by 0.25%.

As the Bank of Canada rate moves, interest rates on banking products offered by financial institutions, including EQ Bank, will often shift as well.

Will I still earn bonus interest with qualifying direct deposit transactions?

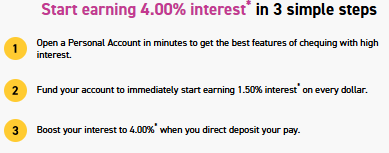

While the base rate for Personal Accounts and Joint Accounts will be 1.50%*, the bonus interest rate for customers with eligible direct deposits will increase to 2.50%*. Customers who continue to meet the requirements of the offer will earn a total of 4.00%* interest.

We have updated our EQ Bank Bonus Interest Offer Terms and Conditions to reflect this interest rate change. To view these updated terms and conditions, click here.

Will I still get a 2% match for my TFSA, RSP, and FHSA contributions?

Any new contributions made between November 1 and February 28 will still be eligible for the 2% match.** Click here to view the EQ Bank Registered Savings Match Promotion Terms and Conditions.

Is there anything I have to do?

There’s no action required on your end. The new rates take effect on February 4, 2025, and will be automatically applied to your account. Your interest payment on March 1, 2025, will be reflective of the current rate from February 1 to 3 and the new rates from February 4 to 28.

We’re committed to providing you with some of the best interest rates in Canada with no monthly bank fees. If you have any questions, our Customer Care team is available to help from 8:00am to midnight ET through live chat.

Sincerely,

EQ Bank

7:38 pm

September 28, 2023

Offline

I was pondering moving my DD over to them to get the 3.5%, but I think the 4% might be the motivation I need. I wonder why they are incentivizing DD so much, when it seems like they have no fees from day-to-day banking to grab back from us. Will this bonus last, or is this just to get new signups for a while?

Any opinions from those who are using EQ as their daily account?

8:34 pm

April 6, 2013

Offline

No fees for us. But, 1.44% or 1.55% Mastercard interchange from the merchant when one spends with the EQ Bank card, a prepaid Mastercard.

That 1.44%+ is more than the 0.95% or 1.22% interchange from a World Mastercard in-person tap or chip spend.

The PC Money account has a similar setup.

I suspect the bonus will last if many account holders spend the direct deposited funds through the EQ Bank card. Pay 4% per annum but collect potentially 1.44% per two weeks (37.44% per annum) on each pay spent!

9:53 pm

September 28, 2023

Offline

Aha! Great insight Norman... so that would be the same reason Wealthsimple dangled $100 to me a few months ago to switch DD to them. I guess I could be one person that might hurt the bonus... I use CC's that have more attractive rewards, and just bill pay them from my daily account. I also don't like using a card that can be used online that is linked to my daily account, though it seems EQ has a good setup of having a separate card balance from the main account (one can basically define their own credit limit that way).

11:43 pm

April 21, 2022

Offline

everhopeful said

Aha! Great insight Norman... so that would be the same reason Wealthsimple dangled $100 to me a few months ago to switch DD to them. I guess I could be one person that might hurt the bonus... I use CC's that have more attractive rewards, and just bill pay them from my daily account. I also don't like using a card that can be used online that is linked to my daily account, though it seems EQ has a good setup of having a separate card balance from the main account (one can basically define their own credit limit that way).

WS allows you to open multiple Cash accounts and then select which one you wish to attach the card to for spending. It's fast and simple to quickly transfer and withdraw funds from the card. I don't keep much funds in the Cash accounts, only enough to feed the card. When I need more for spending, I'll e-Transfer funds to a WS Cash non-card account as required. You can select which account is to be used for deposits. WS provides a unique personal email address which can be used for auto-deposits of e-Transfers.

11:55 pm

September 28, 2023

Offline

I do have WS set up that way, but I hardly keep any funds in savings there because I do not trust their 10x CDIC protection scheme. I feel much more comfortable keeping large balances with EQ bank because they are a direct member of CDIC as Equitable Bank.

8:35 am

August 4, 2010

Offline

FWIW, I've got an EQ savings account, but never received the 4% email, and I still see a banner on my EQ dashboard mentioning the 3.5% offer. The account just started getting DD deposits again in January, and the bonus rate won't kick in again until next week for me. Not sure that they would have targeted the email to existing bonus folks only, though, as they don't seem to be doing any sort of Tangerine varying offers.

In any case, I was chatting with an agent about something else, and they confirmed the 4% combined bonus rate starts tomorrow (typing "bonus interest" in their chatbot also mentions "4%".

9:01 am

April 6, 2013

Offline

The e-mail (around January 30) was a general "Our interest rates are changing on February 4, 2025" and didn't seem to be an e-mail for a targeted offer.

The February 4 start date (tomorrow) is probably why their web site still says 3.50% for those who set up direct deposit:

9:52 am

April 6, 2013

Offline

The 4% rate is online now:

* Interest is calculated daily on the total closing balance and paid monthly. For the EQ Bank Card, interest is paid into the linked Personal Account. Rates are per annum and subject to change without notice. For the Personal Account, Joint Account and EQ Bank Card, the current base interest rate is 1.50% (the “Base Rate”). Customers who add and maintain qualifying recurring direct deposits of at least $2000/month to a Personal Account or Joint Account are eligible to earn a bonus interest rate of 4.00% (the Base Rate plus an additional 2.50%) for the eligible accounts (the Personal Account, Joint Account, and the EQ Bank Card balance). Conditions apply. Please review the EQ Bank Bonus Interest Offer Terms and Conditions for details.

7:05 pm

January 10, 2017

Offline

Norman1 said

No fees for us. But, 1.44% or 1.55% Mastercard interchange from the merchant when one spends with the EQ Bank card, a prepaid Mastercard.That 1.44%+ is more than the 0.95% or 1.22% interchange from a World Mastercard in-person tap or chip spend.

The PC Money account has a similar setup.

I suspect the bonus will last if many account holders spend the direct deposited funds through the EQ Bank card. Pay 4% per annum but collect potentially 1.44% per two weeks (37.44% per annum) on each pay spent!

With so many credit cards with better benefits, how many people want a card that gives .5% cashback and is pre-paid so no short-term loan period? Likely, people with no savings. I wonder what % of the card carrying population would want this?

10:05 pm

December 4, 2016

Offline

Many companies are in the hunt for Direct Deposits.

Direct Deposits are a easy way to attract more money with time.

Like Simplii and the 500 dollars they offered in the recent past and other banks with offers like this.

I think those took a chunk out of the EQ base of Direct Depositors. Than they see Wealthsimple's credit card requiring it, to have no annual fee and they are a bit behind and needing to catch up with what other banks are dangling out there.

It's good as it increases competition and makes banks offer better incentives. They are not trying to increase the client base with the 4%. They are trying to stop the loss of Direct Deposit money, mainly from Wealthsimple's new credit card product. Which is likely to attract many EQ clients to Wealthsimple in terms of Direct Deposits. Once most people switch their direct deposit, I think they will not change it back unless incentivized. Even if incentivized I do not think most would switch back.

1:50 am

November 18, 2017

Offline

Pre-paid cards are sold exclusively for people who have crappy credit. The claim is that you can repair your credit. The reality is they get your cash FREE and STILL charge you interest if you incur it - despite already having your money!

RUN away from these. If you need to repair your credit, just about anyone can get a Candian Tire Card. Make sure you get it from Corporate - the shills wandering the store will give you a card that's a much worse deal.

RetirEd

9:28 pm

April 6, 2013

Offline

Lodown said

With so many credit cards with better benefits, how many people want a card that gives .5% cashback and is pre-paid so no short-term loan period? Likely, people with no savings. I wonder what % of the card carrying population would want this?

Definitely not much appeal in the EQ Bank Card's ½% back for someone who has and successfully manages a credit card that gives more back, like 2% back for certain purchases and 1% back on the rest. That's really not the intended market for the EQ Bank Card.

There doesn't need to be appeal to a large percentage of the card holding population for the EQ Bank Card to be successful for its issuer. Instead, EQ Bank needs to attract enough people, not necessarily a significant share of the market, who will deposit funds into their EQ Bank Personal Account and then spend enough of the funds through the EQ Bank Card. There is that 4% interest rate for those who set those deposits up as regular, automatic direct deposits of pay or pension.

Remember the spread: Up to 4% per annum interest paid. Up to 37.44% per annum in interchange earned.

Also, not everyone who has money can manage a credit card properly. Instead, they end up having to pay 18%+ per annum on a balance they cannot pay at the end of each month. Reloadable, prepaid cards are a good alternative for such people.

9:53 pm

December 4, 2016

Offline

It is a good fx card the EQ bank card.

0.5% plus no 2.5% = 3% difference from most ccs.

It adds up if your spending thousands. It is a small difference if you spend hundreds.

I use the EQ bank card more than the Home Trust Visa with no 2.5 percent off.

I have used the EQ bank card to take money out from bank machines. They reimbursed each time. Nice feature.

The card is a good tool to help people with problems spending to stop spending. As you set how much is in there. If you go over it will decline you. Where as a credit card or debit card would likely allow you to go deep into the red without much warning signs.

Most people have some issue with spending or over spending. I mean the amount of people that have a addiction to gambling always amazes me. Horse race gambling, Casinos, Sports gambling, you can almost gamble on anything these days as well, gambling over the internet.

One of the biggest issues within a relationship is usually involving spending of some sort.

Credit cards are only useful if you can control your spending.

Cash, cards like this eq card. Force people to control their spending. Most people are not so in tune with what there spending. I would guess most that participate in these forums are mostly checking or over checking. Which is not the normal person.

12:25 am

April 14, 2021

Online

Online

User230 said

The card is a good tool to help people with problems spending to stop spending. As you set how much is in there. If you go over it will decline you. Where as a credit card or debit card would likely allow you to go deep into the red without much warning signs.

Sounds like an ideal card for online purchases. You can set the limit for only legitimate purchases and protect yourself from any unauthorized purchases, if your credentials are stolen.

Please write your comments in the forum.