Log In

Log In Register

Register Home

Home

Topic RSS

Topic RSS

Facebook

Facebook Twitter

Twitter Email this

Email this4:01 pm

December 12, 2009

Offline

Offline

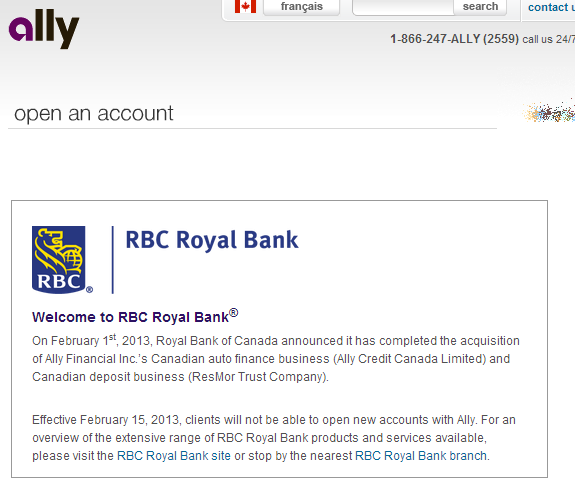

RBC Royal Bank has moved quickly since announcing on February 1st, 2013, that they have completed their acquisitions of the Ally Credit Canada Ltd. automobile financing and ResMor Trust Company ("Ally.ca") deposit businesses. As expected, they continued to utilize the Ally platform to allow customers access to their high-interest savings accounts, TFSAs and GICs as well as perform account maintenance transactions. However, on Friday, February 15th, 2013, they announced via their continously updated FAQ site that as of that date, no further Ally Canada deposit accounts (including high-interest savings accounts, GICs, TFSAs and U.S. dollar savings accounts) could be opened for both existing Ally Canada customers as well as non-customers, effectively announcing the winding down of Ally Canada and ResMor Trust Company operations. Existing customers can, however, continue to use "ally.ca" to maintain their existing accounts but no further GIC renewals would be permitted either.

(See screenshot below.)

Simultaneously, RBC also announced (via the ResMor Trust Company website) that GICs and term deposits currently sold through deposit brokers would no longer be able to be opened. As existing GICs/term deposits mature, they would not be able to be renewed and would be paid out back to the customer (presumably via Electronic Funds Transfer or Canadian bank draft).

I predicted RBC would take this route for its deposit operations as it did not show any interest in rejuvenating the products and seemed singularly focused on its auto financing business to grow its own consumer loans and dealer floor plan financing books. I'm just surprised they're doing it this quickly - they clearly have no interest in even trying to migrate Ally savings accounts and GICs to the RBC platform and, from the ResMor dealer notice above, the same will be true of Ally GICs that come up for maturity, they will either be paid out to one's own Ally savings account or via EFT or Canadian bank draft to another Canadian bank account. I now also suspect that RBC will accelerate the winding down of Ally Canada deposit operations by reducing the interest rate to 0%, to help clients either open RBC savings accounts or transfer out to another financial institution in much the same way Citizens Bank of Canada did several years ago with their high-interest savings accounts. It's sad to see RBC doing this but they clearly thought it would be too much work to try and retain the very small value of deposits that Ally Canada/ResMor Trust Company had (something like $2.5 billion CAD or less; at their peak, they exceeded only Canadian Tire Financial Services in market share by deposits) and, unlike with Scotiabank's acquisition of ING Direct which came with something like $25-30 billion CAD in deposits and roughly that amount in mortgages, RBC doesn't need to do anything to try and retain that business whereas Scotiabank paid a substantial sum and must retain as much business as it can. Also, remember that last year, ResMor Trust Company sold its mortgage portfolio and servicing operations to MCAP so it really only had deposits (GICs and savings accounts) left. The real value was in the Ally Canada consumer auto financing and dealer floor plan financing and subsidized auto loans (called "subvented loans" or something like that).

With this news, I strongly urge Peter to remove Ally from the "comparison chart" as soon as practicable. As well, once the final closure of Ally's deposit operations is given or after a period of six months, whichever comes first, my ask is that the Ally forum here be locked to prevent future threads being added. As well, to replace Ally on the chart, I strongly encourage Implicity Financial to be added forthwith, both to the comparison chart and with forum & profile created (more on Implicity's response to my questions coming in a separate thread). ![]()

Cheers,

Doug

Footnote: See ResMor Trust Company's latest balance sheet filing, with OSFI:

http://www.osfi.gc.ca/WebApps/.....lData.aspx

5:34 pm

December 23, 2011

Offline

While Citizens did provide the option to move your funds and mortgages to TD, keep in mind that Citizens was not bought out by another bank. Citizens was owned (and still is) by Vancity CU and apparently Citizens was going to be kept to manage Vancity's Visa and apparently they are still alive but deal with investment brokers only.

If Citizens came back in the same form that they were .... wow that would be fantastic!!!

If you look at the history of Ally .. they did not come from good roots. RBC just bought some of their competition which allows RBC to continue to gouge their customers.

6:34 pm

December 12, 2009

Offline

I don't know why the takeaway from my post was the comparison to Citizens Bank of Canada. Obviously, it's not an absolute comparison that is directly correlated but if you look in a general sense, Citizens Bank sold their mortgage and secured line of credit portfolio to TD, wound down GICs as they matured, changed the high-interest savings account rate to 0% and then sold their unsecured LOC and chequing account portfolio to their parent entity, Vancity, and closed down savings accounts. They no longer operate any investment or deposit products whatsoever, maintaining only a small commercial mortgage portfolio and a foreign exchange payments division as well as a prepaid Visa credit cards unit. In actual fact, it is very similar. ![]()

At any rate, with the above announcement and news, Ally definitely needs to be removed from the "comparison chart" and, eventually, have its forum "locked". Implicity Financial is a great candidate to replace it and no further discussion is needed on that as I think everyone here is in support of that. ![]()

Cheers,

Doug

6:39 pm

February 16, 2013

Offline

Hello Doug,

Thank you for the update on Ally - much appreciated. That is why I love this site so much; I am always up to date. My preference would be to keep Ally on the chart until such time as their interest rate becomes the lowest on offer. In that way, I will be able to keep tabs of what is occurring.

I agree that the interest rate may be lowered to 0% in one fell swoop but until that happens, I will keep my money where it is. I need time to figure out what my next best option is. I really liked Ally's platform allowing the user to push and pull funds with ease and will miss this feature immensely. ![]()

Regards,

MG

10:23 am

May 15, 2007

Offline

Wow, that did not take very long for RBC to start winding down Ally Financial. Thanks for sharing, Doug. I agree that it should be removed from the comparison chart since no new accounts can be opened.

I will add Implicity soon. I'd like to wait a bit more to see if we can get some discussion with people who have opened an account with Implicity. In the meantime, I've create an Implicity Financial forum.

4:15 pm

December 23, 2011

Offline

Doug said

I don't know why the takeaway from my post was the comparison to Citizens Bank of Canada. Obviously, it's not an absolute comparison that is directly correlated but if you look in a general sense, Citizens Bank sold their mortgage and secured line of credit portfolio to TD, wound down GICs as they matured, changed the high-interest savings account rate to 0% and then sold their unsecured LOC and chequing account portfolio to their parent entity, Vancity, and closed down savings accounts. They no longer operate any investment or deposit products whatsoever, maintaining only a small commercial mortgage portfolio and a foreign exchange payments division as well as a prepaid Visa credit cards unit. In actual fact, it is very similar.

At any rate, with the above announcement and news, Ally definitely needs to be removed from the "comparison chart" and, eventually, have its forum "locked". Implicity Financial is a great candidate to replace it and no further discussion is needed on that as I think everyone here is in support of that.

Cheers,

Doug

My apologies.

Peter

6:35 pm

December 12, 2009

Offline

Peter - Thanks for acting quickly and removing Ally from the "comparison chart". Anytime a product is no longer available for sale or an orderly wind down of operations is commenced should warrant its immediate removal, in much the same way you acted swiftly to remove Citizens Bank of Canada's Ultimate Savings Account or the former HSBC Direct Savings Account. I'm sorry if I sounded abrupt or excited in some way; I just think it's a good policy to follow. Again, thank you. ![]()

As for adding Implicity Financial to the comparison chart, the reason I thought we should skip a lengthy vetting / comment process that is normally required (and a good policy I might add) is because it already offers a well-known online banking platform in MemberDirect (which Canadian Western Bank, Assiniboine Credit Union's Outlook Financial and Westoba Credit Union's MAXA Financial all use and of which all are already part of the "highinterestsavings.ca" comparison chart), is available to Quebec residents, has even less service fees than the other Manitoba-based credit unions and pays the highest rate of interest in Canada. You're quite right that we should normally allow for greater public comment and discourse - I was only trying to comment that I would be supportive of us skipping (or curtailing) that process in this case, if you wanted to. I apologize if any disrespect was felt.

Peter (kanaka) - I didn't know you and Peter K. (the forum administrator) shared the same name. No apology is necessary at all. Again, I, too, am sorry if my reply to you seemed abrupt or disrespectful in any way. I just wanted to point out my comparison to Citizens Bank of Canada may not have been a "true" apples-to-apples comparison but was using it as I felt it was still pretty good in terms of the process that RBC was taking with Ally Canada vis a vis Vancity took with Citizens Bank of Canada.

Regarding Implicity Financial, I've started the "account opening" process and plan to shut down my Ally accounts in the near future and perhaps even shut down my Hubert Financial account. I'm excited to use the MemberDirect platform as I have never had an account with a financial institution that uses that system. That said, I, too, (in reference to MG's post here) will miss Ally's push/pull self-to-self transfer. I'm hoping Implicity will offer the automated, "paperless" small "test" deposit external account verification method like Ally and Hubert Financial did. It is, nonetheless, important to streamline and close account(s) I'm no longer using or will be demised. Implicity Financial provided some answers to my initial questions on January 25th, but since starting the account opening process today (Feb. 17th), I've replied with some additional questions and will keep you all posted. For now, here are the response(s) to my initial questions (my questions are in bold text with Erin Johnson's, Contact Centre Supervisor, responses in italic text):

1. I'm assuming that like other Manitoba-based credit unions operating virtual banking divisions, all deposits are guaranteed/insured by the Manitoba Deposit Guarantee Corporation. You need to become a "member" of Entegra Credit Union and I'm assuming, correct me if I am wrong, that Entegra will either pay for your membership share (provided you return it to Entegra when your membership is cancelled) to become an Implicity Financial customer. You can be a resident of any Canadian province with a valid Social Insurance Number and external chequing/savings account from a Canadian financial institution to become a "member" of Implicity Financial/Entegra Credit Union. Do I have all of this correct?

Our deposits are 100% guaranteed by the Credit Union Deposit Guarantee of Manitoba. All new members of Implicity Financial require a $5 deposit into a Common Share account. As long as your accounts are open for 6 months, the $5 will be returned to you upon closing your accounts with us. Yes you are correct, Implicity Financial is open to all Canadian Residents who are over the age of 18 with a valid Social Insurance Number. We require each new member to send us an initial cheque deposit written on a Canadian financial institution with their name and address imprinted on it as well as their signature. This will act as your signature card on file.

2. Do you perform a so-called "soft" inquiry (non-credit-related inquiry that is not disclosed to other credit grantors/inquirors and has no impact on one's own credit score) one's Equifax or TransUnion consumer credit report or a "hard" inquiry (credit-related inquiry that is disclosed to other credit grantors/inquirors and may impact one's own credit score)? As a supplemental question, do you use either Equifax or TransUnion, or both, to perform said inquiries and, if both, are both "soft" or "hard" inquiries?

During the application process we ask a few identification questions which are pulled from your bureau but it’s a “soft” inquiry. During our administration process we run the credit bureau as a “hard” inquiry. The “soft” inquiry is with TransUnion and the “hard” inquiry is with Equifax.

3. Regarding ATM deposits, I'm assuming you're not a member of The EXCHANGE Network but are a member of the Canadian Credit Union Network known as Acculink and, as such, can make surcharge-free deposits or withdrawals through the Acculink ATM network, correct?

We aren’t a member of the Exchange Network but we are part of the Acculink Network. With that said, all deposits and withdrawals done at a Canadian Credit Union ATM machine are free.

My note: You can access the credit union ATM (Acculink) locator and download an app for iOS/Android/BlackBerry devices at the recently launched site: http://www.ding-free.ca

4. In terms of hold policies, what is the hold period (if any) on ATM deposits and EFT transfers in from other financial institutions in one's own name where the transfer in was requested from the Implicity Financial side of things? If different hold periods for the different methods, please specify both. Do you provide any sort of "access to deposited funds"/"cash back" limits for well-established clients, clients with significant holdings/deposits with Implicity Financial or clients with good credit scores/reports whereby only amounts above a certain threshold are held for your standard hold period? If so, what is that threshold and does this exception apply to both ATM and EFT deposits/transfers in or just ATM deposits?

All ATM deposits, cheque deposits and EFT transfers are held for 10 business days.

5. I love your website and your online banking platform seems to either use, or at least partially incorporate some of, MemberDirect platform, or technology, is this correct? If so, that's awesome! If not, what platform/technology do you use?

We do use the MemberDirect platform for our online banking. We also use a security feature called Increased Authentication which provides another layer of security to your login process. When you first log in, you'll be asked to select an image, write a security phrase, and select three security questions.

6. Do you have any sort of "member referral" program whereby you can identify an existing member so they receive some sort of "perk" or "incentive"?

Right now we don’t have any sort of “member referral” program.

Cheers,

Doug

8:33 am

May 15, 2007

Offline

The latest news: all Ally savings accounts will be closed on April 30, 2013:

http://www.rbcroyalbank.com/al.....index.html

Funds will be transferred to the linked account on file or mailed as a cheque.

8:15 am

February 20, 2013

Offline

Yes, the regular Ally accounts will be closed end of April. The TFSAs won't but, as could have been expected from RBC, they already dropped the interest rate to 1.2%.

I moved my TFSA money out at the end of December (to avoid fees and delays) because they dropped their rate to 1.8% to avoid the transfer fees and have them now at Achieva at 2%. Feel sorry for those not paying attention and who now are stuck with a return of 1.2% unless they are willing to fork over around $100 or more to transfer to another FI where they can still get the 2%.

Which reminds me, don't bother moving your money by having the FI do it, even if there are no xfer fees involved. It takes weeks before the money is transferred and you will get diddly-squat on it during that time. They actually told me that they "send a cheque" to the other FI, rather than doing an electronic xfer.

On the Manitoba CUs hold issue, I still cannot fathom why there is a 10 business day hold on electronic transfers. We are in the 21 century for crying out loud! If the money was not there I could not have transferred it. What is this hold for. It is all done electronically. I have questioned these absurd delays with several banks and never received a plausible answer. The 10 day hold seem to be a Manitoba thing though. Most FIs elsewhere will take 5 days or less.

6:41 pm

December 12, 2009

Offline

Thanks for posting the update on the closure, Peter. It also sounds like access to the "ally.ca" online banking platform will cease after April 30th, 2013 as well. GICs and TFSAs will continue but likely with no online access.

Rick has posted an update on the Ally rates over in this thread and in my reply, I've expanded on that and provided additional analysis and rational, logical speculation here. I thought I'd link to these great posts rather than continuously cross-posting everything. So, I encourage everyone to read and comment in that thread as well.

Frugal - completely agree with you on the 10-day holds at the Manitoba CUs being unreasonable. Unfortunately, they aren't regulated by FCAC and the provincial financial services commissions provided minimal regulation basically around share capital and incorporation rules. In terms of running their business, it's like banking was 50 years ago - minimal regulation and oversight in terms of consumer protection! We are starting to see some credit unions routinely refuse to open accounts for clients with no credit history or poor credit scores, which is unfortunate as they have typically helped the disadvantaged and stayed in small communities without any banks.

In terms of TFSAs, the reason they are likely keeping them is they are registered products and harder to transfer. That said, after April 30th, 2013, you won't have any online access to these accounts. What I could potentially see RBC doing is allowing people to transfer out their TFSAs with no transfer fee – or waiving the transfer out fee when you transfer it to a TFSA product from a member of the RBC Financial Group. Cue the "big bank" cynicism! ![]()

I have e-mails into Ally and will post details soon as well as any promotional offers I get in the postal mail (have only received an e-mail from RBC so far).

Cheers,

Doug

8:41 am

February 22, 2013

Offline

National Post (Theresa Tedesco) has an excellent analysis here:

http://business.financialpost......-business/

Greg

2:08 pm

December 12, 2009

Offline

Here's a follow-up e-mail between me (Feb. 17th; in bold) and Implicity Financial (Feb. 19th; in italics):

I'm curious, as no application for a credit facility or access to funds (i.e., overdraft/line of credit or immediate access to deposited funds such as no holds), why is it necessary for you to perform two (2) credit inquiries (one "soft" one with TransUnion and one "hard" one with Equifax)? You should have full access to one's TransUnion consumer credit report and be able to view any sort of personal identification, active/closed credit facilities and any recent inquiries on one's credit file from that. Both Hubert Financial, a division of Selkirk, MB-based Sunova Credit Union, and ING Direct Canada, a subsidiary of The Bank of Nova Scotia, only pull a "soft" inquiry for all online account openings in order to satisfy their own internal as well as regulatory/anti-money laundering requirements. In order to limit the number of recent inquiries on my consumer credit reports, my ask of you is that since I am not applying for credit nor am I asking for any special reduced hold times on deposits is that you only use my TransUnion consumer credit report to fulfill your administrative requirements involved in the account opening process. Also, could you pass on this as a suggestion to your head office/operations department in charge of developing your account opening policies & procedures manual that the TransUnion inquiry be used for both the identity verification questions in the online account opening questionnaire but also in any & all administrative procedures to actually open the account(s), provided the application is not seeking a credit facility or reduced hold times on deposits?

The “soft” inquiry through TransUnion doesn’t affect your bureau (beacon score) any way. That inquiry is run for security purposes for when members complete the application process. Once we receive the physical cheque for your initial deposit we run the “hard” bureau using Equifax which does affect your beacon score. We don’t see any of the security questions asked by TransUnion therefore we need to run the credit bureau on our end once we receive the deposit. So unfortunately all members need to have their credit bureau run when opening an account. This is required through our anti-money laundering legislation.

In terms of the ATM and EFT deposit hold times, can you pass on a second suggestion to reduce these times, in line with the major Canadian chartered banks and most credit unions (i.e., for ATM deposits, 4-5 business days after the day of the deposit and, for EFT deposits/transfers in, 2-3 business days from the date the transfer in request is made)? This would be in line with ING Direct Canada, Hubert Financial and Ally Canada, a product/division of ResMor Trust Company.

Our policy for holds is 10 business days. If a member brings in multiple deposits which clear with no issue we may be able to reduce the hold days, but for all new members we place 10 day holds.

Finally, I had only one more question I forgot to ask: does your online banking platform allow Implicity Financial customers to add other Canadian bank accounts in their own name using the one or two small "test" deposit verification method? For instance, let's say I add my ING Direct Canada THRiVE Chequing Account to my Implicity Financial online banking profile, in order to verify my ING Direct Canada Account, Implicity Financial would send a small "test" deposit (or two) less than $1.00 to that account and then I go into Implicity Financial online banking to key in the amount of the small "test" deposit once it shows up in that account in order to validate the account. This is the way Hubert Financial and Ally Canada allow you to add external Canadian bank accounts and is a much simpler, more streamlined (and paperless!) verification method than sending in a paper-based form with a VOID cheque or VOID cheque/account verification form/original bank statement from that external Canadian financial institution.

As of right now our two ways to transfer electronically are through Interac E-transfer which cost $1.50 per transaction and Electronic Funds Transfers which are set up using our Pre-Authorized Transfer form and attaching a void cheque which can then be emailed or faxed to us. I have attached the link for the form https://www.implicity.ca/SharedContent/documents/PreAuthorizedTransferform.pdf

In the upcoming months we will be providing members the access to transfer funds from one institution to Implicity and vice versa through their online banking. We also offer cheques and ATM cards to our members.

I also asked, "One more quick question (I promise!) - can I change my Implicity Financial debit card PIN at an Acculink Network ATM?", which went unanswered, and forgot to ask when Implicity Financial actually launched publicly but will re-ask/ask those questions in my fourth message to them.

This prompted another follow-up between me and Kerrie Dobson, Contact Centre Representative, on Feb. 22nd as Erin was out of the office:

As for the second, "hard" credit bureau check you perform through Equifax, that shouldn't be a problem. Although I had an inquiry at the end of December 2012, other than that I've had no "hard" inquiries in over a year so shouldn't affect it too much. I'm hoping you'll retain a copy of my credit bureau report for as long as I have an account/membership with Implicity Financial, in case I ask to see it in the future, it won't be necessary to pull it again. My suggestion, however, is that you run a second, "soft" credit bureau inquiry with TransUnion (instead of Equifax) to fulfill your account opening/anti-money money laundering regulatory requirements. This would be in line with what Canadian Direct Financial (part of Canadian Western Bank), Hubert Financial (part of Sunova Credit Union) and ING Bank of Canada are already doing. Could you kindly pass this along to the appropriate department?

Erin is away today, so I’ll respond on her behalf. We will retain a copy of your bureau with your file for as long as your account remains open, so there should be no need to run an additional inquiry in the future.

Second, in terms of the ATM/EFT holds, the hold periods on new members is understandable. However, I would like for you to pass on a second suggestion to the appropriate department charged with implementing changes to your policies & procedures that your standard EFT hold period be 2-3 business days, which would be consistent with what the "virtual bank" competition is doing. For ATM deposits, I'd like to see the maximum ATM deposit for all clients be a maximum of 7 business days for all CAD deposits (cash or cheques, since, let's face it, most FIs use an outsourced provider with no way of notifying you of cash deposits). Or, are you saying that if that provider notifies you of a cash deposit by an Implicity Financial member, you'll reduce the hold period? At any rate, if you wouldn't mind passing on this second suggestion, it would be greatly appreciated.

The 10 day hold period was put into place to safeguard both our members and Implicity against any type of fraudulent activity on accounts. We are not notified as to what an ATM deposit consists of, so we are unable to amend hold periods based on cash vs. cheque deposits.

In terms of the EFT transfers, and forgive me if this sounds a bit rushed as I am just heading off to work but wanted to get this e-mail in, does that mean you can currently do sporadic EFT transfers online once you link your external bank account using the pre-authorized transfer form or do you only allow a regular savings plan of a specified amount? In terms of the future plans for a online verification/account linking method, does that mean we'll be able to use the small "test" deposit method? If so, that's great.

Our EFT Transfers are to be used for regular deposits to your Implicity account of a specified amount, which we can set up on our end. We are working towards having the linked account functionality available by the summer, and at that time will have more information for you regarding the small test withdrawal.

As you can see, they are very responsive and very helpful. I will have to follow-up, though, as they seem reluctant to pass on my suggestion(s) for procedural/efficiency improvements regarding credit bureau checks and hold periods to their appropriate operations team. As well, I'd like to see the regular/standard hold period for all deposits (even if no "access to deposited funds"/"cashback" limit(s)) reduced to 7 business days and 2-3 business days for EFT transfers where the funds are "pulled" in once they offer that service, which they currently don't offer as the pre-authorized payment form is only for regular, fixed amount automatic transfers between an external account and Implicity Financial. Does everyone else have the same take/read on that?

It is also interesting they will be launching the account verification method similar to Hubert Financial and Ally but will be using "a small, test withdrawal," not a deposit, which makes sense as the same information is included in the EFT transfer as a deposit but without the extra cost to them. I just hope they deposit that small withdrawal into one's Implicity Financial account so we're not out any money. I will follow-up with them once it actually launches. We may even see more FIs use this method as well. ![]()

Cheers,

Doug

2:27 pm

December 12, 2009

Offline

GSmall99 said

National Post (Theresa Tedesco) has an excellent analysis here:

http://business.financialpost......-business/

Greg

Thanks for sharing this, Greg. Sounds like Theresa's analysis is very much what I've been preaching and prognosticating here.

A little more from me on this topic and then I'll be done before I sound like I'm "beating a dead horse". ![]()

I think what you'll see in terms of Scotiabank buying ING Direct's Canadian assets & RBC buying Ally's Canadian assets (and she's right on the money [no pun intended] on this point) is Scotiabank needing them to "bulk up" on deposits to boost their capital adequacy ratios whereas RBC took Ally's Canadian assets solely for the huge consumer auto and dealer floor plan financing to essentially became a leader in a new business line and were quite likely forced to take Ally's ResMor Trust Company deposit business (i.e., sort of like saying, "I'll sell you my yacht but you have to take this little aluminium fishing boat that goes with it.") and that's why you're seeing the very quick winding down of the small deposit business to get it over quickly as it was very likely a money losing operation. I feel for the call centre employees, most of whom have already likely received some sort of notice of severance or will in the future. ![]()

We've seen RBC's plans unfold and, down the road in the months ahead, is GICs will gradually be rolled over into RBC issued GICs using the RBC platform but they may retain the ResMor Trust Company entity for CDIC purposes or they may decide to liquidate it entirely and close it up to save on CDIC membership dues & deposit insurance premiums. In terms of Scotiabank buying ING Direct's Canadian assets, you'll see potential future plans for ING Direct Canada rebranded as something like Scotia Direct, Scotia Money, RED Bank or some other name now that ING Direct USA has been rebranded as Capital One 360, a sort of "direct banking" operation with the tagline/slogan, "the national bank of wherever," that is a separate unit of Capital One Bank which has some branches. Scotiabank may tweak the ING Direct Canadian products around the edges, possibly allowing ING Direct Canadian customers to have full-access to Scotiabank's ATM network instead of The EXCHANGE ATM Network to save on costs & so forth but, if they do that, they will disconnect from The EXCHANGE ATM Network as they will not want the extra burden of having to process other FIs deposits and bill payments at what would then be the largest Exchange ATM Network member in Scotiabank. They'll most likely launch a no-fee and/or low fee credit card, probably a Visa card and not the hoped for MasterCard, now that they've partnered with American Express to give them dual issuer status. They'll probably expand the line of credit/overdraft offering, may institute a nominal fee for WHOOPS! protection and likely expand/enhance the Mutual Funds product portfolio. In short, like RBC needing to grow consumer auto financing, Scotiabank needs to organically grow this multi-channel deposit business.

Cheers,

Doug

10:40 am

February 22, 2013

Offline

Doug:

I read an article about Capital One's purchase of US based ING and the consensus was that Capital One made a huge blunder by not including the ING tradename in the purchase.

US banking is fragmented 1000 times more than Canadian and while ING and the orange colour had established a presence the feeling was that Capital One were "starting over".

I was also in to see my RBC contact Friday and she had lots of info from head office on Ally's car loan business but knew absolutely ZERO on their deposit business.

I also received the RBC mailed "offer" and was hard pressed to find anything in it that wasn't in the email, which basically said, "come to RBC's 1.2% HISA".

Greg

10:53 am

December 12, 2009

Offline

GSmall99 said

Doug:

I read an article about Capital One's purchase of US based ING and the consensus was that Capital One made a huge blunder by not including the ING tradename in the purchase.

US banking is fragmented 1000 times more than Canadian and while ING and the orange colour had established a presence the feeling was that Capital One were "starting over".

I was also in to see my RBC contact Friday and she had lots of info from head office on Ally's car loan business but knew absolutely ZERO on their deposit business.

I also received the RBC mailed "offer" and was hard pressed to find anything in it that wasn't in the email, which basically said, "come to RBC's 1.2% HISA".

Greg

Hi Greg:

One - Capital One DID use the ING Direct USA tradename for above 12 months (believe the acquisition closed in mid-late 2011) or so, maybe a bit less than Scotiabank's agreement with ING Groep but they had to change the name eventually. Capital One They did, however, acquire the Sharebuilder tradename so will continue using that name indefinitely. Scotiabank will have to ditch the ING Direct Canada tradename by May 2014 at the absolute latest. I expect them to start the rebranding by October or November 2013, though, which is a good thing as I'm sick of the ING brand already. It's doing nothing for them. Keep the "forward banking" motto if they want, but start fresh and put massive marketing dollars into it.

Two - sounds like you're in agreement with me on RBC basically being forced to take Ally's deposit business - they probably didn't even really want it! LOL ![]()

Cheers,

Doug

3:38 pm

December 12, 2009

Offline

You'll be please to know I received my initial "account activation e-mail" from Implicity Financial on Feb. 25/2013 (after mailing in my initial deposit cheque on Feb. 18/2013; five business days prior). I have since sent a subsequent e-mail to Implicity Financial staff on Feb. 24/2013 and received a response back Feb. 23/2013, the full of text of which and subsequent follow-up discussion continues here.

All future correspondence and Implicity Financial account opening discussion will continue there.

Cheers,

Doug

Please write your comments in the forum.